Category

Accounting

5 min. read time

What is a balance sheet?

The balance sheet is a central component of accounting and serves to present a company’s financial position at the end of a fiscal year. It includes all assets and equity items that were acquired or sold during the fiscal year, as well as outstanding receivables and liabilities. Its main purpose is to determine the difference between a company’s assets and liabilities.

Why is accounting important?

Financial reporting provides companies with a comprehensive overview of their assets and is an essential tool for assessing a business’s financial health. It documents all business transactions and thus provides management with important information about the company’s financial position and the trends in its profits and assets. It also serves as a guide for strategic decision-making and is of great importance to potential lenders. It enables them to better assess the opportunities and risks associated with granting a loan.

Together with the income statement, the balance sheet also constitutes the annual financial statements required by the German Commercial Code (HGB), which merchants and companies required to use the double-entry bookkeeping system must prepare.

What does a balance sheet look like?

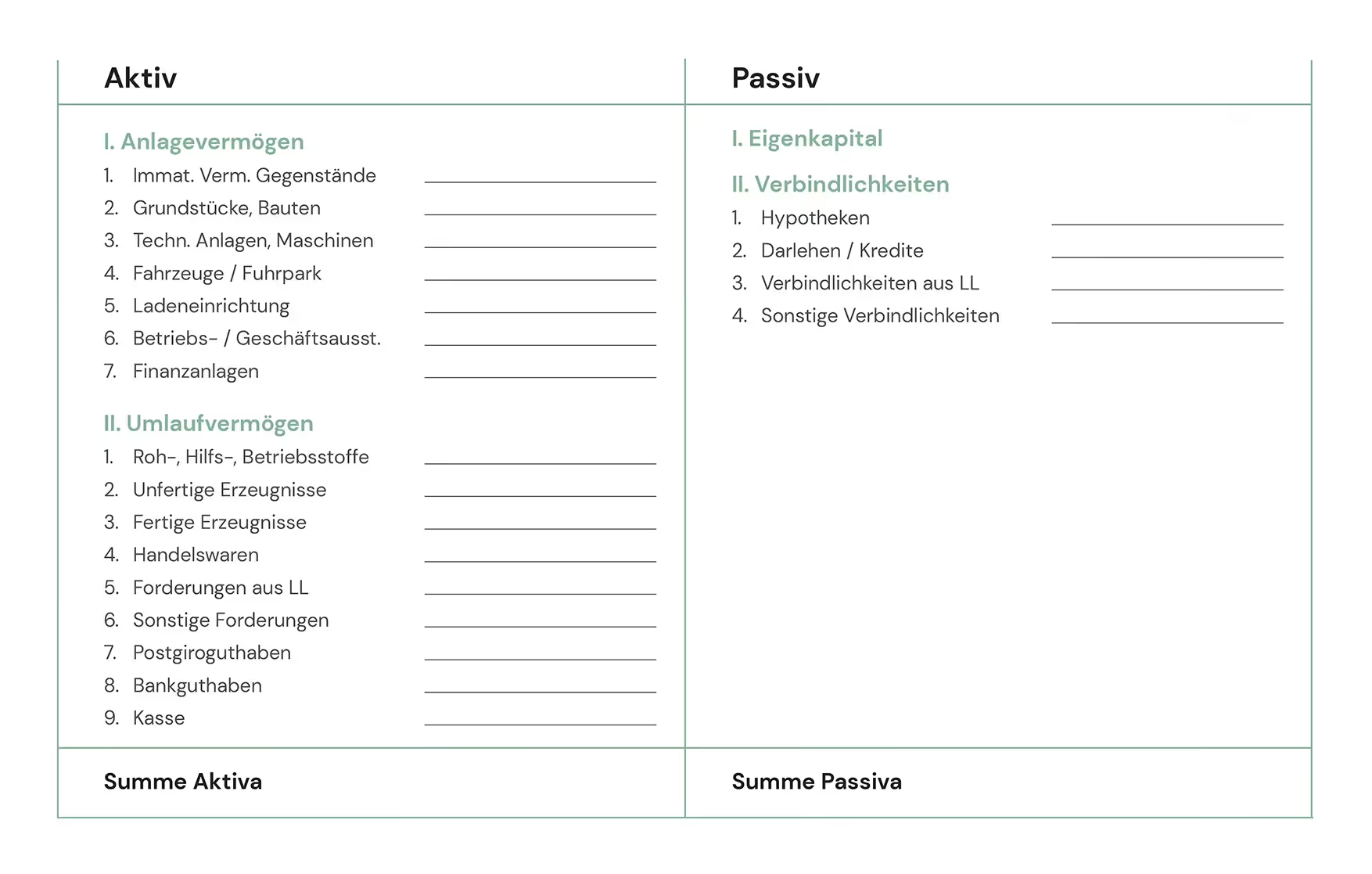

Accounting is based on the principle of double-entry bookkeeping, in which a balance sheet is divided into debits and credits, or assets and liabilities . Assets represent the company’s assets, while liabilities represent its debts. While assets are listed on the left side of the balance sheet, liabilities are listed on the right. The balance sheet equation states that the sum of all assets must equal the sum of all liabilities, so that the financial resources on the assets side are always covered by the corresponding sources of financing on the liabilities side. If the total assets ever exceed the total liabilities, a net income is reported; in the opposite case, a net loss is reported. This balances the total assets and liabilities.

Assets are divided into fixed assets and current assets. Fixed assets include long-term investments such as buildings, machinery, and company vehicles, while current assets include short-term assets such as inventory, cash and cash equivalents, and securities. As a general rule, fixed assets take precedence over current assets, since long-term investments form the basis of business operations.

Liabilities include equity and debt and show the source of the funds received. Equity represents the shares held by the business owners or shareholders. It may also consist of the owners’ personal assets that they have contributed to the company. Borrowed capital, on the other hand, consists of debt. It refers to financial resources made available to a company by banks, investors, suppliers, or partners for its operations. In addition to liabilities, borrowed capital also includes provisions. Companies must set these aside to create reserves for the future or for investments.

Because of the risk that equity poses to owners, it is reported on the balance sheet above liabilities. If losses occur or the company becomes insolvent, debts to creditors are paid first before equity is tapped.

The balance sheet format pursuant to Section 266 of the German Commercial Code is as follows:

What does accounting under the German Commercial Code (HGB) mean?

The German Commercial Code (HGB) requires companies that engage in commercial activities and operate a business organized on a commercial basis to prepare an annual balance sheet. It also specifies how a balance sheet must be structured and prepared. Specifically, it must be prepared in accordance with generally accepted accounting principles, which require, among other things, clarity, accuracy, and completeness. In addition, it must be prepared in German and signed by the authorized persons. The currency in which a balance sheet must be prepared in Germany is the euro. Pursuant to Section 266 of the German Commercial Code (HGB), the presentation requirements specify which items must be included in the balance sheet and where they must be recorded. Different requirements apply to the balance sheet depending on the legal form and size of the company. However, most companies must prepare their balance sheet in accordance with the HGB in account form, listing assets, liabilities, and the balance sheet total. Exceptions may apply to freelancers and small business owners under certain conditions.

Who is required to prepare financial statements?

The legal requirement to prepare financial statements in Germany applies to companies that engage in commercial activities and operate a business organized on a commercial basis. This includes sole proprietorships, corporations, and partnerships, although the latter are not required to publish their financial statements in the Federal Gazette. In principle, commercial enterprises whose nature and scope require them to operate a business in a commercial manner are obligated to use double-entry bookkeeping and, consequently, to prepare annual financial statements that include a balance sheet. Sole proprietorships and partnerships whose annual revenue and profit do not exceed the thresholds of 600,000 and 60,000 euros, respectively, in two consecutive fiscal years are exempt from the requirement to prepare a balance sheet under Section 4(3) of the Income Tax Act (EStG). In such cases, they may use a simplified accounting method—the income-excess method (EÜR)—to determine their profit instead of preparing a balance sheet. This also applies to businesses not registered in the Commercial Register, such as sole proprietorships and civil law partnerships (GbR), as well as to self-employed professionals, regardless of their revenue and profit.

Practical Steps for Preparing a Balance Sheet in Accordance with the German Commercial Code (HGB)

Preparing a balance sheet in accordance with the German Commercial Code (HGB) requires a clear sequence of steps to ensure that it complies with legal requirements. Here are the basic steps that guide this process:

• Recording of assets and liabilities: This involves recording all of the company’s assets and liabilities, including fixed assets, current assets, equity, and debt.

• Compliance with presentation requirements: The presentation requirements under Section 266 of the German Commercial Code (HGB) provide clear instructions on the separation of liabilities and assets, as well as on the detailed listing of these items in the balance sheet. They also govern the calculation of equity as the difference between assets and liabilities.

• Preparation of the balance sheet: After the data has been recorded and prepared, the actual balance sheet is prepared. In this process, assets and liabilities are reported in full, taking into account the statutory presentation requirements.

• Review by professionals: To ensure compliance with legal requirements, the balance sheet should typically be reviewed by qualified accountants or tax advisors.

Interim Support

Does your finance team need help?

Book a no-obligation initial consultation now.

Schedule a meeting

Additional Resources